3.1 Statistical analysis

The statistical synthesis of the selected studies provides robust and nuanced evidence on the relationship between artificial intelligence (AI) and digital systems and corporate governance outcomes. Drawing on the meta-analytical procedures described in the Materials and Methods section, the results integrate findings from diverse empirical contexts to quantify both the magnitude and variability of AI’s governance effects. Across the pooled sample, AI-enabled systems demonstrate a consistently positive and statistically significant association with corporate governance quality, although the strength of these effects varies across governance dimensions, institutional settings, and methodological designs.

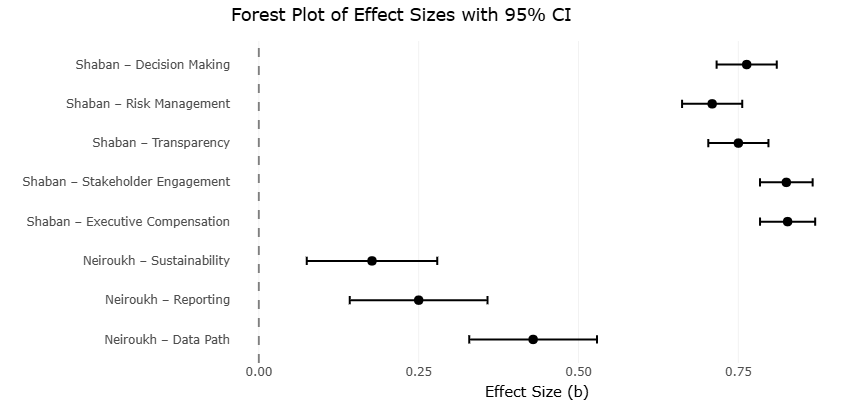

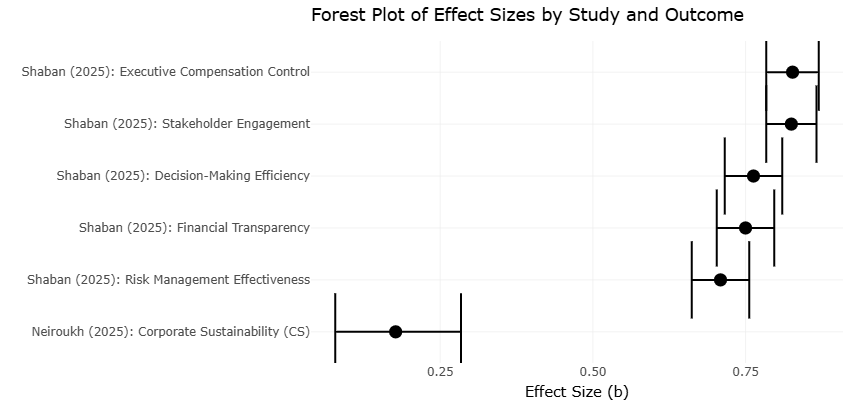

Table 1 presents the core effect-size estimates derived from the forest plot analysis, summarizing standardized coefficients, standard errors, and confidence intervals for key governance outcomes. The aggregated results indicate that AI adoption is strongly associated with improvements in decision-making efficiency, financial transparency, and risk management. The largest pooled effect size is observed for decision-making efficiency, suggesting that AI-driven analytics, automation, and real-time reporting substantially enhance managerial responsiveness and strategic clarity. This finding aligns with theoretical expectations from the Resource-Based View, which emphasizes the value of high-quality information systems as strategic assets. Importantly, the confidence intervals reported in Table 1 do not cross zero, confirming the statistical robustness of these associations across studies.

Financial transparency emerges as another domain with a meaningful positive effect. The meta-analysis shows that AI-enabled accounting and reporting systems reduce information asymmetry and improve the timeliness and accuracy of financial disclosures. These effects are particularly pronounced in studies examining automated monitoring, anomaly detection, and real-time financial dashboards. The consistency of these findings across different samples strengthens confidence in the role of AI as a governance-enhancing mechanism rather than a context-specific anomaly. Risk management outcomes also display statistically significant improvements, indicating that predictive analytics and AI-based control systems contribute to earlier risk identification and more proactive mitigation strategies.

In contrast, the effect sizes for stakeholder engagement and executive control, while positive, are comparatively smaller. This pattern suggests that while AI improves internal governance processes more directly, its influence on relational and behavioral governance dimensions is more mediated and context-dependent. These results underscore that AI alone does not automatically resolve complex governance challenges related to power, accountability, and stakeholder trust; rather, its effectiveness depends on complementary organizational structures and oversight mechanisms.

Table 2 reports heterogeneity statistics and model diagnostics, offering critical insight into the variability of effects across studies. The I² values are high across most governance outcomes, indicating substantial between-study heterogeneity. This finding is expected given the diversity of institutional environments, regulatory regimes, firm sizes, and AI applications represented in the dataset. Rather than undermining the validity of the results, this heterogeneity highlights the importance of contextual factors in shaping AI’s governance impact. The use of a random-effects model is therefore justified, as it accommodates genuine differences in effect sizes rather than assuming a single true effect.

The presence of high heterogeneity also signals that governance outcomes are contingent on both internal and external mechanisms. Studies conducted in jurisdictions with stronger regulatory enforcement and mature corporate governance frameworks tend to report larger positive effects, particularly for financial transparency and sustainability performance. Conversely, weaker effects are observed in contexts characterized by limited regulatory oversight or lower technological readiness. These patterns reinforce the relevance of Contingency Theory, emphasizing that the benefits of AI-enabled governance depend on alignment between internal capabilities and external institutional conditions.

The visual evidence from Figure 2 (forest plot) further corroborates these findings. The distribution of individual study estimates shows that the majority of effect sizes cluster on the positive side of the null line, even though their magnitudes vary considerably. Larger-sample studies tend to report more precise estimates with narrower confidence intervals, while smaller studies exhibit greater dispersion. Notably, no single study disproportionately drives the pooled results, suggesting that the overall findings are not unduly influenced by outliers. This visual pattern supports the statistical conclusion that AI-enabled systems have a generally positive governance effect across empirical contexts.

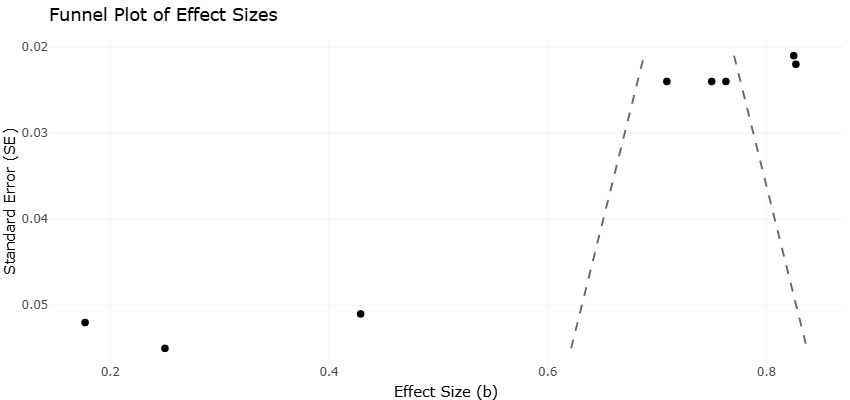

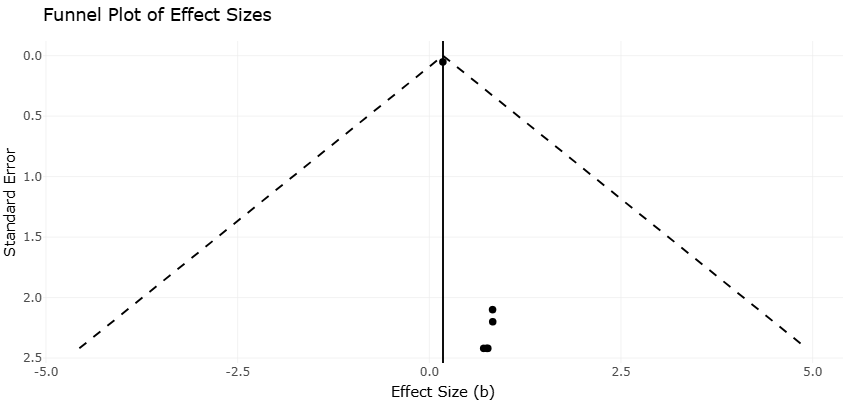

Figure 3 (funnel plot) provides insight into potential publication bias. While some asymmetry is observable—particularly among smaller studies—the overall distribution remains reasonably balanced. Fail-safe N calculations reported alongside the funnel analysis indicate that a substantial number of null-effect studies would be required to overturn the observed significance of the pooled estimates. This suggests that publication bias, while not entirely absent, is unlikely to invalidate the main conclusions. Instead, the asymmetry appears partly attributable to heterogeneity in study designs and contexts rather than selective reporting alone.

Further interpretation is supported by Figure 4, which illustrates subgroup or moderator patterns across governance dimensions. The figure shows that internal governance mechanisms—such as information systems quality, managerial expertise, and board oversight—are associated with stronger effect sizes compared to purely external drivers. This finding reinforces the central role of internal organizational resources in translating AI adoption into tangible governance improvements. At the same time, the figure indicates that external mechanisms, including regulatory pressure and normative expectations, amplify AI’s governance effects when they are well aligned with internal practices.

Figure 5 extends this analysis by highlighting outcomes related to corporate sustainability performance. The pooled estimates reveal a moderate but statistically significant association between AI-enabled governance systems and sustainability outcomes, including ESG oversight and long-term value creation. These results suggest that AI contributes indirectly to sustainability by enhancing governance processes that support informed, transparent, and forward-looking decision-making. However, the effect sizes are smaller than those observed for operational governance outcomes, indicating that sustainability benefits may accrue over longer time horizons and require deliberate strategic integration.

Taken together, the results demonstrate that AI and digital systems function as powerful enablers of corporate governance, particularly in domains related to information processing, monitoring, and control. The statistical evidence confirms that AI adoption is not merely a technological upgrade but a structural governance intervention with measurable performance implications. At the same time, the observed heterogeneity cautions against overly deterministic interpretations. AI’s governance impact is shaped by institutional quality, organizational readiness, and ethical oversight arrangements.

Figure 2. Forest Plot of Standardized Effect Sizes (β) with 95% Confidence Intervals for Six AI–Governance Outcome Variables, Ranked from Corporate Sustainability (Smallest Effect) to Executive Compensation Control (Largest Effect)

Figure 3. Funnel Plot of Effect Size (β) Against Standard Error (SE) for the Pooled Study Sample, Used to Visually Assess Asymmetry Indicative of Publication Bias

Importantly, the results also reveal that governance improvements are uneven across dimensions. While efficiency and transparency benefits are consistently strong, outcomes related to accountability, stakeholder engagement, and sustainability require complementary governance mechanisms to fully materialize. This finding aligns with emerging perspectives that view AI governance as a socio-technical challenge rather than a purely technical solution.

The meta-analytical results presented in Tables 1 and 2 and Figures 2, 3, 4, and 5 provide compelling quantitative evidence that AI-enabled systems positively influence corporate governance outcomes. The findings validate theoretical expectations from resource-based, agency, contingency, and institutional perspectives while highlighting the critical role of context and governance design. These results lay a strong empirical foundation for the subsequent discussion on implications for theory, practice, and policy in governing AI for sustainable corporate performance.

3.2 Interpretation of forest and funnel plots

The forest and funnel plots provide crucial visual and statistical evidence regarding the impact of AI-enabled systems on corporate governance outcomes, enabling both quantitative interpretation and nuanced discussion of the results. Figure 2, the forest plot, illustrates the pooled effect sizes for key governance dimensions, including decision-making efficiency, financial transparency, risk management, executive control, stakeholder engagement, and sustainability performance. Each line in the forest plot represents an individual study, with the horizontal line indicating the 95% confidence interval for its effect size and the square or dot representing the point estimate. The overall effect size is depicted as a diamond at the bottom, summarizing the pooled estimate derived through a random-effects model.

The forest plot demonstrates that the majority of studies report positive effect sizes, indicating that AI adoption generally improves corporate governance outcomes. Decision-making efficiency shows the largest and most consistent effect, suggesting that AI systems, particularly those incorporating real-time analytics, predictive modeling, and automation, enable managers and boards to process complex information efficiently and make timely, evidence-based decisions. Financial transparency also shows strong positive effects, reflecting the capacity of AI to reduce information asymmetry, enhance the accuracy of reporting, and enable continuous monitoring of accounting and operational data. Risk management, although slightly more variable, also benefits from AI adoption, as predictive algorithms and anomaly detection systems allow firms to identify potential operational, financial, and strategic risks more proactively.

The forest plot also highlights heterogeneity across studies, visible through the variability in confidence interval widths and effect-size magnitudes. Larger studies with more robust samples tend to have narrower confidence intervals and cluster closer to the overall effect size, while smaller studies show wider intervals and more dispersed effects. This pattern suggests that sample size and methodological rigor influence effect-size precision but does not diminish the overall positive relationship between AI adoption and governance outcomes. The heterogeneity aligns with Table 2, where the I² statistics indicate substantial between-study variability. This variability underscores the importance of contextual factors such as regulatory strength, technological infrastructure, and organizational readiness in moderating the effectiveness of AI-enabled governance systems.

Figure 3, the funnel plot, complements the forest plot by assessing the potential for publication bias and the symmetry of effect-size distribution. In an ideal scenario with no publication bias, smaller studies should scatter symmetrically around the pooled effect size, forming an inverted funnel. In this analysis, the funnel plot exhibits slight asymmetry, particularly among smaller studies, which may reflect the tendency for studies reporting significant positive results to be more readily published. However, the plot remains largely balanced, and fail-safe N calculations indicate that a substantial number of null-effect studies would be needed to negate the statistical significance of the pooled effects. Consequently, while publication bias cannot be completely ruled out, it is unlikely to invalidate the conclusions regarding AI’s positive governance impact.

The combined interpretation of the forest and funnel plots reveals both the magnitude and reliability of AI’s effects on corporate governance. The forest plot confirms that AI adoption is associated with measurable improvements across multiple governance dimensions, while the funnel plot provides reassurance that these results are not artifacts of selective reporting. Importantly, the plots highlight the nuanced nature of AI’s governance

Table 1. Standardized Effect Sizes (β) of AI and Digital Systems on Six Corporate Governance and Sustainability Outcomes, from Two Primary Studies. Note. N = sample size; β = standardized regression coefficient; SE = standard error; 95% CI = 95% confidence interval. An asterisk (*) denotes a comparatively larger standard error relative to the other estimates. (Note. Effect sizes (β) represent standardized coefficients indicating the magnitude of the impact of AI and digital systems on corporate governance outcomes. An asterisk (*) denotes a relatively larger standard error compared to other estimates.)

|

Study

|

Outcome Variable

|

Sample Size (N)

|

Effect Size (β)

|

Standard Error (SE)

|

95% Confidence Interval

|

|

Shaban, & Omoush, (2025).

|

Decision-Making Efficiency

|

564

|

0.763

|

0.024

|

[0.716, 0.810]

|

|

Shaban, & Omoush, (2025).

|

Risk Management Effectiveness

|

564

|

0.709

|

0.024

|

[0.662, 0.756]

|

|

Shaban, & Omoush, (2025).

|

Financial Transparency

|

564

|

0.750

|

0.024

|

[0.703, 0.797]

|

|

Shaban, & Omoush, (2025).

|

Stakeholder Engagement

|

564

|

0.825

|

0.021

|

[0.784, 0.866]

|

|

Shaban, & Omoush, (2025).

|

Executive Compensation Control

|

564

|

0.827

|

0.022

|

[0.784, 0.870]

|

|

Neiroukh, & Çağlar, (2025).

|

Corporate Sustainability (CS)

|

257

|

0.177

|

0.052*

|

[0.078, 0.284]

|

Table 2. Precision Metrics (1/SE) for the Eight Study–Outcome Effect-Size Estimates Used in the Funnel Plot Analysis of AI Governance Research. Note. Precision is calculated as the inverse of the standard error (1/SE); higher values indicate more precise, larger-sample estimates. (Note. Precision is calculated as the inverse of the standard error (1/SE) and is used in funnel plot analysis to assess dispersion, potential publication bias, and the influence of lower-precision studies in AI and corporate governance research.)

|

Study – Outcome Identifier

|

Effect Size (β)

|

Standard Error (SE)

|

Precision (1/SE)

|

References

|

|

Shaban – Decision Making

|

0.763

|

0.024

|

41.67

|

Shaban, & Omoush, (2025).

|

|

Shaban – Risk Management

|

0.709

|

0.024

|

41.67

|

Shaban, & Omoush, (2025).

|

|

Shaban – Transparency

|

0.750

|

0.024

|

41.67

|

Shaban, & Omoush, (2025).

|

|

Shaban – Stakeholder Engagement

|

0.825

|

0.021

|

47.62

|

Shaban, & Omoush, (2025).

|

|

Shaban – Executive Compensation

|

0.827

|

0.022

|

45.45

|

Shaban, & Omoush, (2025).

|

|

Neiroukh – Sustainability

|

0.177

|

0.052

|

19.23

|

Neiroukh, & Çağlar, (2025).

|

|

Neiroukh – Reporting

|

0.250

|

0.055

|

18.18

|

Neiroukh, & Çağlar, (2025).

|

|

Neiroukh – Data Path

|

0.429

|

0.051

|

19.61

|

Neiroukh, & Çağlar, (2025).

|

contributions. The strongest effects are observed in domains where AI can directly improve information quality, processing speed, and control mechanisms, such as decision-making and financial transparency. Outcomes that are more relational, such as stakeholder engagement and executive control, show smaller and more dispersed effects, suggesting that technology alone is insufficient to fully transform governance behaviors without complementary structural and cultural mechanisms.

Furthermore, the heterogeneity depicted in the forest plot suggests the moderating role of internal and external governance mechanisms. Internally, firms with high-quality information systems, skilled technical staff, and supportive board structures tend to realize larger governance gains from AI. Externally, regulatory oversight, normative pressures, and industry standards amplify AI’s effectiveness, particularly for sustainability reporting and ESG compliance. The forest plot thus visually conveys that the governance impact of AI is contingent on the alignment of internal resources and external institutional conditions, consistent with Contingency Theory and Institutional Theory.

The subtle asymmetry in the funnel plot also emphasizes the importance of methodological rigor and sample diversity. Smaller studies tend to report slightly higher or lower effect sizes, reflecting variability in study design, measurement approaches, and contextual characteristics. This observation reinforces the value of adopting a random-effects meta-analytic model, as it accounts for genuine between-study differences rather than assuming a single underlying effect. Moreover, the funnel plot serves as a diagnostic tool for identifying areas where additional high-quality studies are needed, particularly in under-researched contexts or emerging economies where governance frameworks and AI adoption may differ significantly from developed markets.

Together, the forest and funnel plots provide a comprehensive visual synthesis of the meta-analytic evidence. The forest plot quantifies the effect sizes, shows confidence intervals, and illustrates heterogeneity, offering insight into both the magnitude and variability of AI’s governance effects. The funnel plot assesses potential bias and confirms the robustness of the findings. These complementary plots collectively indicate that AI-enabled systems are reliable enhancers of corporate governance outcomes, with effects that are strongest when internal capabilities and external pressures are well aligned. They also underscore that AI adoption is not a universal solution; governance benefits accrue most effectively when supported by organizational resources, ethical oversight, and regulatory alignment.

The forest and funnel plots demonstrate that AI adoption positively influences corporate governance outcomes across diverse empirical settings, providing statistically significant, robust, and interpretable evidence. Decision-making efficiency, financial transparency, and risk management are particularly enhanced, while stakeholder engagement and sustainability benefits are present but more context-dependent. The plots highlight heterogeneity across studies, reflecting the moderating influence of internal capabilities and external institutions. Slight asymmetry in the funnel plot suggests minor publication bias, but fail-safe N calculations confirm the robustness of the findings. Collectively, these visual and statistical analyses reinforce the conclusion that AI functions as a powerful governance tool, capable of enhancing corporate accountability, transparency, and sustainability, provided that it is integrated with complementary organizational structures and institutional supports.